This renewed focus on shareholder returns has emerged because investors are demanding capital discipline. Investors who are willing to engage now are pressing for dividends and share buybacks rather than reinvestment at higher prices. It is likely going to be another 12 to 18 months before we see producers start to reinvest in their businesses while still maintaining a sharp focus on capital discipline and return on investment.

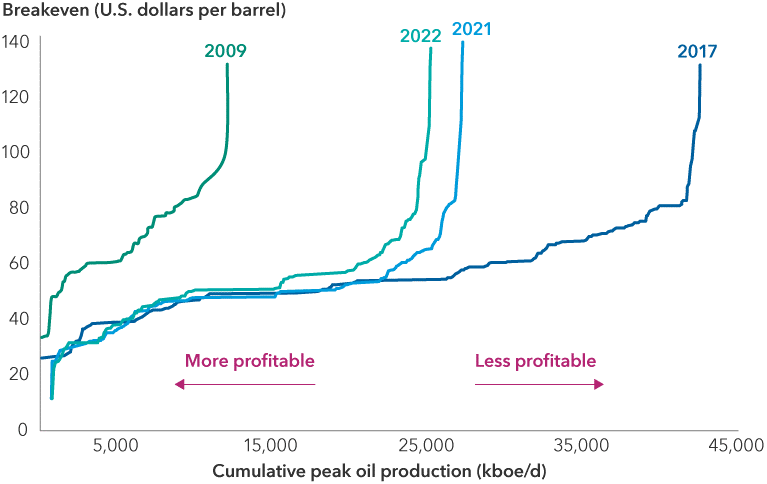

Supply-demand dynamics also support higher oil prices. Widening OPEC+ production deficits and forecasts of dwindling global spare capacity suggest that supply will not catch up to demand for years. Of the major oil-producing countries, Saudi Arabia could increase capacity by a million barrels per day and the United Arab Emirates by another million. But it would take years to build out that capacity, and U.S. production is slowing quite quickly. Taken together, there’s just not enough oil to bolster global supply.

Moreover, exploration costs are going up. Higher quality oil reserves have been used up, and as exploration goes further afield, it gets more expensive and requires greater expertise. U.S. exploration and production companies lack the proficiency for advanced exploration and will likely have to acquire companies that know how to tap into such oil fields to bring new supply to market. Additionally, oil services costs have risen with inflation. While higher costs will impact the entire industry, they’ll most acutely affect smaller companies that have fewer resourcing options.

Taking demand and supply dynamics into consideration, in our view, oil will likely not dip below $70 per barrel under most scenarios, and our analysis shows this would allow the major oil companies to maintain profitability, even when factoring in inflation and higher costs of production.

- What is the impact of the Inflation Reduction Act on energy companies?

The Inflation Reduction Act of 2022 is a landmark piece of legislation. The bill directs $369 billion in federal funding to clean energy tax incentives, loans, and consumer and commercial subsidies that have the potential to improve the return profile in areas such as carbon sequestration and clean hydrogen infrastructure build-out.

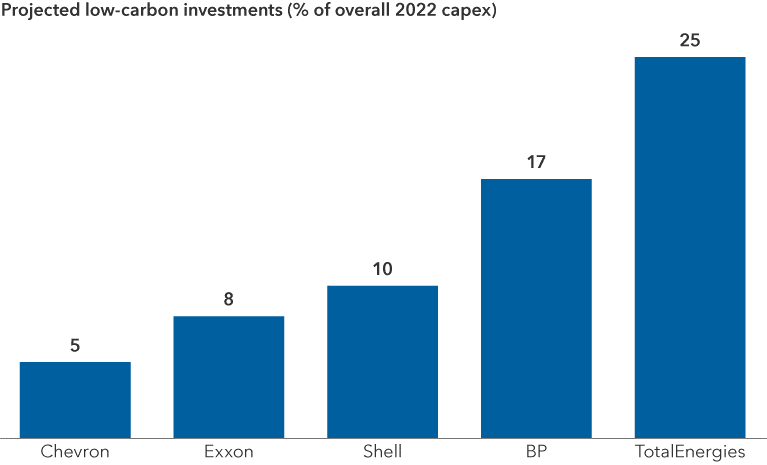

Over the next decade, the legislation could help unleash a wave of capital expenditure. Oil and gas companies, chemical producers and auto manufacturers are among the potential beneficiaries. Only a handful of the U.S. supermajors have scalable low-carbon projects underway, but the subsidies in the Inflation Reduction Act are likely to move others off the sidelines.

Amid the optimism, it’s fair to say that some firms are proceeding cautiously, mindful that policy priorities are often subject to political shifts. While the Biden administration has supported investment in renewables, there’s no guarantee that policy wouldn’t shift back in favor of fossil fuels after the next election or if energy prices become too high.

- How do European and U.S. companies differ in their approaches to decarbonization?

Oil and gas companies, regardless of region, are seeking new ways to reduce emissions in their operations. One of the key drivers of this change in behavior has been the proliferation of net-zero targets, in which new human-produced greenhouse gas emissions are balanced by an equal reduction.

European oil and gas companies are proactively seeking replacements for their fossil fuel businesses, while U.S. companies are primarily focused on removing carbon from their existing businesses. They are leveraging tactics such as carbon sequestration — in which carbon dioxide is removed from the atmosphere and held in solid or liquid form — rather than diversifying their energy mix.

Like their U.S. counterparts, European firms are incentivized by new legislation. The REPowerEU plan, adopted by the European Commission in March 2022, directs nearly 210 billion euros in new investments toward clean energy in the European Union. The bill finances new energy partnerships with renewable and low-carbon gas suppliers, as well as clean hydrogen projects and solar and wind build-outs.